The industrial distribution industry is expanding and evolving, creating challenges that companies must address in order to remain competitive.

By approaching these trends strategically, forward-thinking companies will find opportunities to differentiate themselves in the sector and strengthen customer relationships. Growing value-add services that respond to these trends is key – from expert sales support and digital e-commerce services to environmental target partnerships and expanded service offerings.

Companies can further solidify their success by ensuring supply chain constraints are addressed and finding the right path to follow through consolidation, M&A, and bifurcation of industry players.

In 2022, the revenue of the wholesale trade sector/distributors market topped $8.2 trillion, after increasing 22% from an estimated ~$7 trillion in 2021. With such dramatic growth (though much of that being price driven) and with global and national trends affecting every facet of the industry, distributors looking to succeed in 2023 and beyond must look at the upcoming challenges and develop strategic approaches to address what lies ahead. Everyone understands that these kind of growth rates are not going to continue as robustly as in the past.

Industrial distribution includes a large number of industries and categories (see Figure 1), but across this diverse landscape there are many common themes and challenges, from aging workforces and supply chain disruptions to digital solutions and industry consolidation. While larger players in the space have generally seen higher margins in recent years than other parts of the value chain, addressing these key issues is a necessity to continue growth over the next decade.

Figure 1: Industrial distribution sub-segments

Proliferation of digital solutions

For distributors, the future is now. The proliferation of more advanced technologies such as automation, blockchain, artificial intelligence (AI) and machine learning have enabled distributors to capitalize upon efficiencies created across the value chain, generating sales and margin opportunities. Digital opens possibilities like heightened efficiency, increased customer and partner touchpoints, and the ability to gather data on purchasing behavior.

Driven by customer demand, digital sales channel growth is necessary to respond to shifting consumer needs. 80% of business buyers expect companies to respond and interact with them in real time. Today’s B2B buyers expect that B2C service, and a lack of a strong e-commerce platform can impact revenues and profitability for distributors as a decreasing portion of sales is utilizing in-store support and purchasing.

However, digitization of sales channels must be pursued purposefully – companies need to be digital enough to provide their customers with easy transactions without making it simple for that customer to replace their supplier with a larger e-commerce vendor like Amazon. Distributors can protect against this susceptibility and increase margins by differentiating themselves with value-add factors like consultative sales, industrial knowledge, and tools like inventory management.

Several industrial distribution companies have planned significant investment in their e-commerce sales channels, like Grainger, which increased the percentage of sales initiated through digital channels from 15% in 2005 to 75% in 2021, building out traditional tools with click-to-chat, click-to-call, guest checkout, auto recorder, and mobile applications. Others include Fastenal, which is planning to build out digital capabilities in order to have 85% of its customer spend attributable to digital content, and MSC Industrial Direct, which has grown e-commerce sales with new digital offerings like internet-based vending machines.

Supply chain constraints

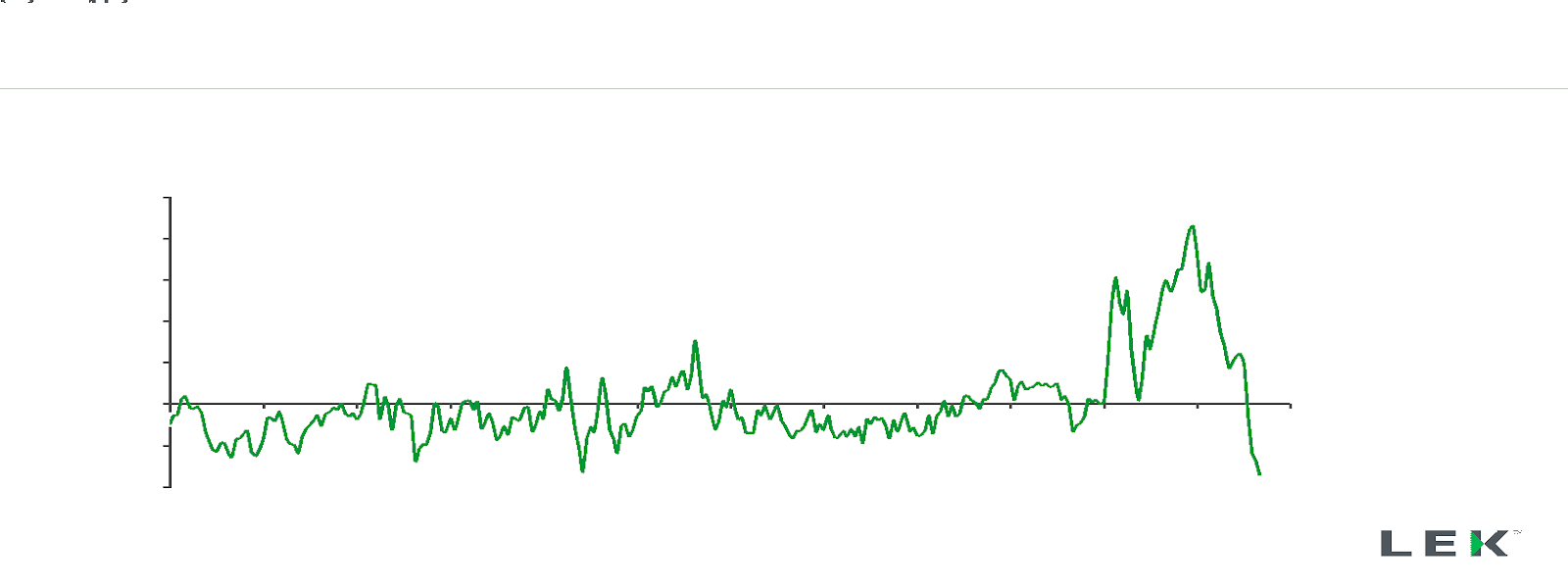

Supply chains have been experiencing disruptions globally due to major events, most significantly the Russia-Ukraine war, inflationary pressures, and the ongoing effects of the COVID-19 pandemic – and industrial distributors have had to rethink their approach to how they interact with them (see Figure 2).

Figure 2: Global supply chain pressure index

Though disruptions from COVID-19 have subsided, they are still a major consideration. Distributors have battled this challenge by increasing sourcing diversity and using more local resources, building extra time into contracts, requiring customers to pay deposits earlier, and pricing in risk of delays. Difficulties resulting from the Russia-Ukraine war have been addressed by diversifying sourcing away from impacted geographies and better forecasting demand and cost for in-demand products. To combat inflation-related challenges, distributors are looking at earlier procurement of products in order to avoid price increases, frequent re-pricing to stay in line with inflation growth, and requiring customers to pay deposits earlier.

Many leading companies have been investing heavily in their supply chains, driving modernization and advanced technology to help in optimization efforts. Most notable among them is Ferguson, which has invested in route planning software, developed features like electronic proof-of-delivery and real-time status visibility to improve customer service, and invested in software, people, and capabilities to accurately forecast and build a demand-driven supply chain. Other investments include Ace Hardware, which has pledged to invest over $800 million into its supply chain over five years targeted at building out retail support centers and implementing a technology platform, and Amazon, which launched the $1 billion Amazon Industrial Innovation Fund to support innovation in fulfilment, logistics, and supply chain.

Outside of these examples, common areas of investment in supply chains include warehouse automation, AI and machine-learning analytics, and cloud-based platform solutions.

Industry consolidation

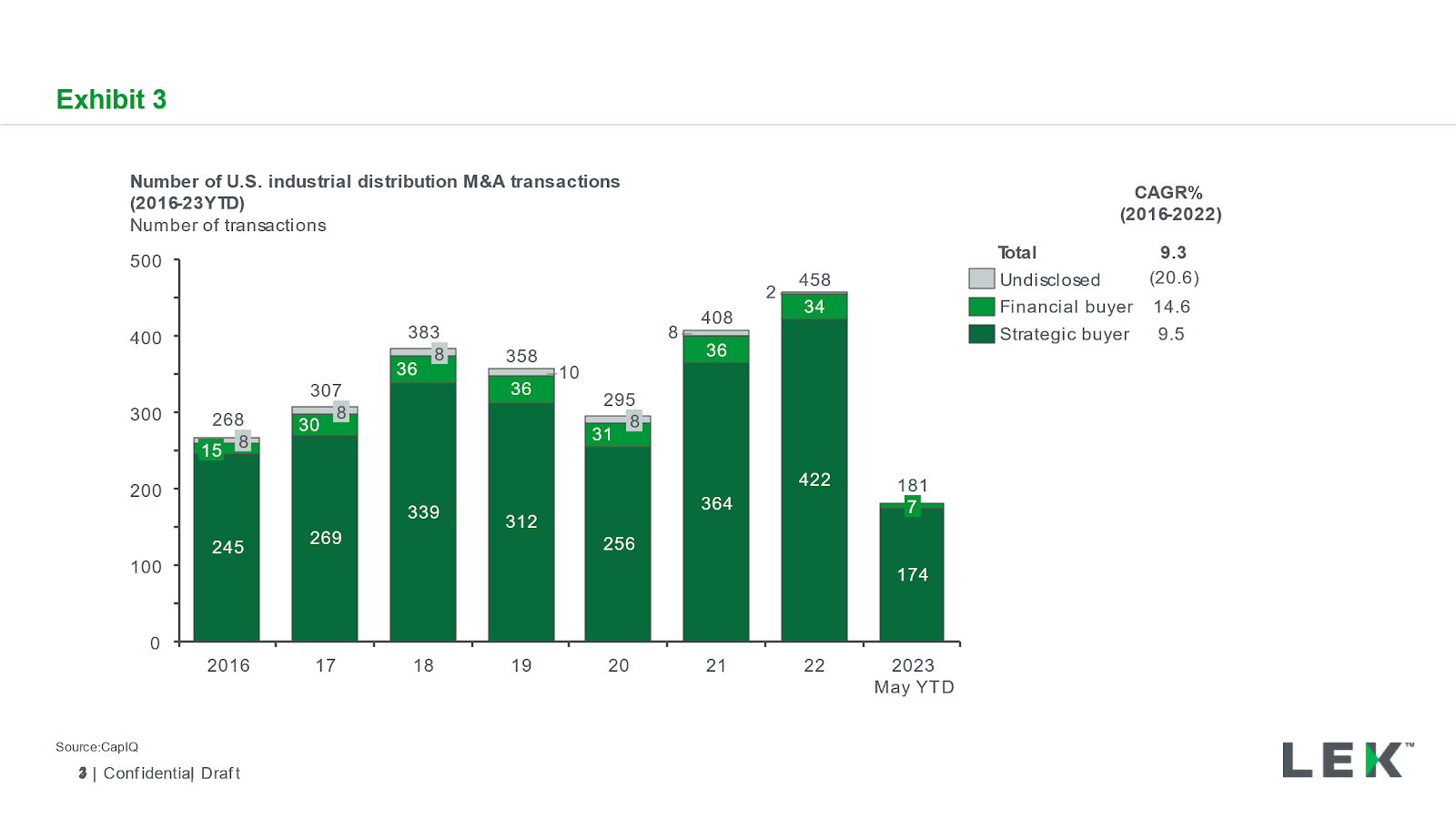

Today’s industrial distribution landscape continues to evolve with ongoing consolidation in the space, as well as increasing bifurcation between broadline and specialized distributors (see Figure 4). Large broadline distributors are expanding into adjacent categories through acquisition, while specialty competitors are increasing their technical expertise and focus.

Consolidation is taking place on several fronts, all combining to increase M&A activity in the space. Broadline distributors have been growing their product breadth and offerings through acquisition, capturing cross-selling opportunities and transforming themselves into one-stop distributors. Specialty distributors have sought their own expansion by acquiring players within their verticals, increasing their expertise and capabilities, broadening their exposure to – and ability to service – more sophisticated customers.

Figure 3: Industrial distribution M&A transactions 2016-23YTD

The industry is also expanding due to the bifurcation among specialty and broadline companies. While large distributors grow by competing on price and breadth of offerings, specialty distributors compete with deep and specialized product offerings, extensive technical expertise, and the ability to support niche clients. This leaves the mid-sized and regional broadline distributors filling the widening bifurcation gap with an uncertain future.

Growth of value-added services

To create new revenue streams and bolster longstanding relationships, industrial distribution companies should seek to differentiate themselves by offering an increasing range of value adds for their partners and customers. With value-added services like inventory management, asset usage tracking, procurement, and enhanced installation, distributors are providing value and increased productivity opportunities for customers as well as covering risks associated with complex supply chains and logistics.

We can see this trend in many current examples of investment. Applied Industrial Technologies has developed a documented value-added service for cost implication data, as well as e-procurement software which allows customers to enhance storeroom management, work order management, and predictive maintenance component scheduling. Fastenal has built a fully integrated distribution network with FASTStock (manual bin stock service enhanced with mobility technology), FASTBin (bin devices with embedded technology for remote inventory monitoring), and FASTVend (specialized devices providing access controls and asset and usage tracking, in addition to remote inventory monitoring).

Aging of the workforce

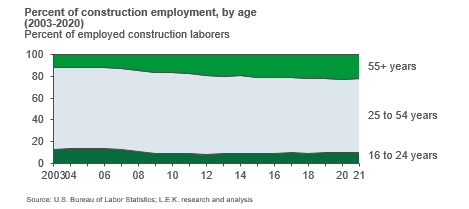

The mixture of an aging workforce – particularly in the realm of contractors – and increasingly complex roles have resulted in difficulties for employers hiring both general and skilled workers. Adding to a shortage of labor, the aging workforce also presents a challenge of institutional knowledge drain – older employees leaving companies take with them years of expertise in both the industry and the company itself that are not easily replaced. The younger contractors that make up the hiring pool are increasingly confident but lack true expertise and capabilities that come with experience (see Figure 4).

Figure 4: Percent of employed construction laborers by age

Distributors have the opportunity to extend their value offerings to customers in the form of incremental contractor support, product training, and purchasing recommendations. As customers become more reliant on the expertise of their distributors, the relationship between the two becomes stronger, increasing margin levels.

Environmental pressures

Industrial firms are feeling pressure from heightened regulatory and public scrutiny around climate and environmental issues, forcing them to reevaluate their approaches to emissions and climate impacts.

One result of that reevaluation is a stronger focus on scope three emissions – increasing attention on emissions up and down the value chain that a company is indirectly responsible for. Using this concept, distributers have an opportunity for differentiating themselves as partners by aiding customers in reaching emissions and climate-related goals. Some ways to do this include minimizing packaging, reducing man hours and energy consumption, and optimizing shipping and last-mile delivery routes.

Determining strategic responses to market challenges

To address these myriad challenges, distributors should reflect on a number of questions to develop strategic responses to oncoming industry changes. These include:

- Value-added strategy: Are we adding sufficient value to avoid disintermediation and by competition by low-cost players?

- Commercial excellence: How do we improve the performance of commercial functions from the go-to-market model through salesforce effectiveness?

- Operational excellence: How do we ensure our organization has the appropriate structure, capabilities, and resources?

- Opportunities for growth: Where can we find opportunities in adjacencies or other parts of the value chain?

- Digital strategy: What digital capabilities will be required to be relevant and successful in the future?

The answers to these will vary based on individual and market circumstances, though L.E.K.’s experience across multiple assignments in this space allows us to determine some common themes. We expect significant interplay between these trends, with all of them contributing to the evolving and growing industrial distribution space.

Through insights gathered while working with clients in the industrial distribution industry, L.E.K. has compiled examples of potential responses to key market trends that may be considered by strategic companies.

Proliferation of digital solutions

- Identify high-impact areas of opportunity for investment in process optimization technologies

- Align with manufacturers’ omnichannel distribution strategies and ensure differentiation in light of proliferation

Supply chain constraints

- Build up redundancy of supply to enable distributor nimbleness in the dynamic supply chain environment

- Enhance information sharing across full value chains, increasing efficiency and avoiding disruptions

Industry consolidation

- Pursue either a broadline or a specialist approach to distribution to avoid being stuck in the middle

- Seek companies with which to partner or to acquire to build out respective offerings and expertise

Growth of value-added services

- Optimize service offerings to increase customer and partner touchpoints by providing value-added services

- Invest in technologies that enable a wider range of value-added service offerings to partners and customers

Aging of the workforce

- Enhance the value proposition to employees and those of distributor customers by increasing range and depth of talent and training resources

- Invest in automation technologies that reduce labor requirements and provide long-term cost advantages

Environmental pressures

- Collaborate with key customers and manufacturers to understand environment-related goals and targets

- Align strategies to clearly define how distributors can provide leverage for partners reducing scope three emissions

Success going forward requires addressing the strategic questions and developing a set of actions in response to trends. The best-honed strategic responses will empower distributors and help them maintain strong channel relationships for both customers and manufacturers amidst change and growth in the industry.

Paul Bromfield, Amar Gujral, Matt Korsch and Alex Rogalski are managing directors at L.E.K. Consulting.